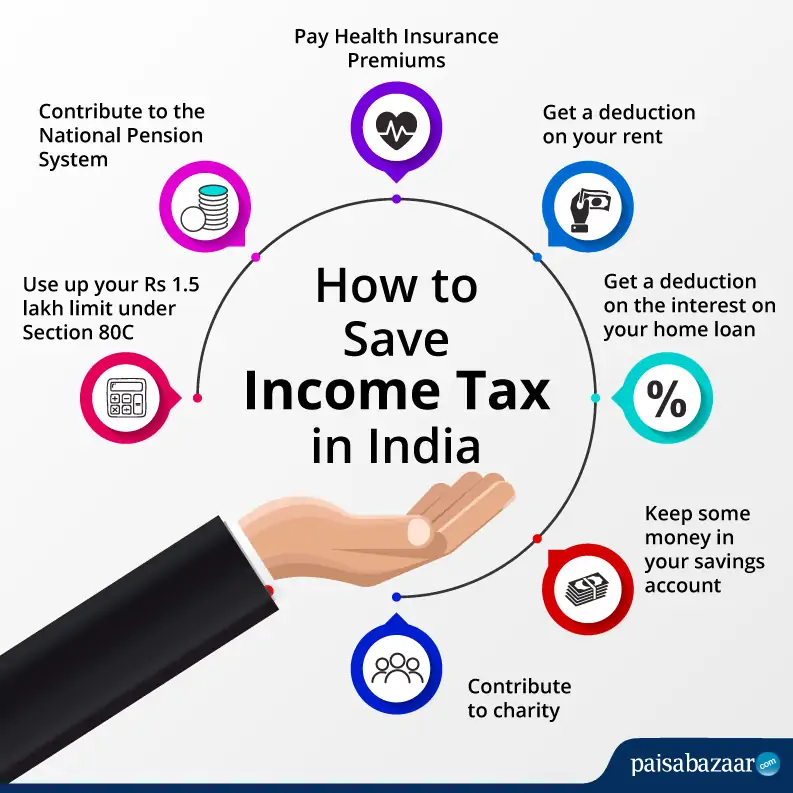

How to Save Tax in India

Rahul Sharma

Finzony Desk

Every year, millions of Indian taxpayers end up paying more tax than they need to — not because the law demands it, but because they simply don't know what deductions are available to them. The Indian Income Tax Act offers a wide range of legal ways to reduce your tax liability, from smart investments to insurance premiums and home loans.

Whether you are a salaried professional, a freelancer, or a business owner, this guide covers everything you need to know about saving tax in India for FY 2025-26.

Old Regime vs New Regime: Which One Should You Choose?

Before diving into tax-saving strategies, you need to decide which tax regime works better for you. India currently offers two options. The Old Tax Regime has higher tax slabs but allows deductions like 80C (up to ₹1.5L), 80D, and HRA. The New Tax Regime has lower slabs but most deductions are not available. Standard deduction is ₹75,000 in the new regime vs ₹50,000 in the old. NPS employer contribution under 80CCD(2) is available in both regimes. Section 87A rebate covers income up to ₹12L in the new regime (zero tax) vs ₹5L in the old.

Rule of thumb: If your total deductions exceed ₹3.75 lakh, the old regime is likely more beneficial. Otherwise, go with the new regime.

Section 80C — Up to ₹1.5 Lakh Deduction

This is the most widely used tax-saving section in India. You can claim a deduction of up to ₹1,50,000 per financial year by investing in ELSS Mutual Funds (best returns, 3-year lock-in), PPF (safe, government-backed, 15-year tenure), EPF (auto-deducted from salary), NSC (fixed returns, 5-year lock-in), Tax-Saver Fixed Deposits (5-year FDs), Life Insurance Premiums, Sukanya Samriddhi Yojana, Home Loan Principal Repayment, and Children's Tuition Fees for up to two children.

Pro Tip: ELSS funds offer the best combination of tax saving and wealth creation. With a 3-year lock-in, they can save you up to ₹46,800 in taxes.

Section 80D — Health Insurance Deduction

Buying health insurance is also a tax-saving tool. You can claim up to ₹25,000 for self, spouse, and children. An additional ₹25,000 for parents below 60 years, or ₹50,000 if parents are senior citizens. Maximum total deduction is up to ₹75,000 per year. You can also claim ₹5,000 within this limit for preventive health check-ups.

Section 80CCD(1B) — NPS Extra Deduction

The National Pension System offers an additional deduction of ₹50,000 over and above the ₹1.5 lakh 80C limit. Combined, Sections 80C and 80CCD(1B) give you a total deduction potential of ₹2 lakh per year. A taxpayer in the 30% bracket can save an extra ₹15,600 just by contributing to NPS.